The post 2020 Taxable Healthcare REIT Dividends appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

Deprecated: parse_str(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-content/plugins/jetpack/class.jetpack.php on line 4222

If you have been paying attention to my “passive income” page, you might have noticed the Max Out of Pocket crew cleared $3,298 in dividends from my medical office building (MOB) REIT experiment in 2020. I sometimes refer to this as my ‘rental’ income. Not bad for a little side hobby.

But how much of that is taxable in 2020?

I initially spread the portfolio out over our taxable brokerage and tax-advantaged retirement accounts. This made things a little convoluted. But for tax purposes, in 2020, all that matters are the dividends that hit my taxable brokerage account.

My Uncle Sam did not tax the dividends in my tax-advantaged accounts in 2020. The ROTH IRA dividends will never be taxed, and the traditional IRA will get taxed like regular income at retirement age. For more on this see: Where do I Keep all of these Medical Office Buildings? I am in the process of simplifying things by closing the positions in my tax-advantaged account. These speculative investments don’t belong there. By the end of 2021, my entire REIT portfolio will be in my taxable brokerage account.

So out of the $3,298 in 2020 REIT dividends, only $1,539 was deposited into my taxable brokerage account. That comes in at just under 47% of the total.

But how much tax did we have to pay on that $1,539?

Taxable REIT Dividend Break Down

Coming in at $1,539, the dividend distributions in my taxable account are up a staggering 733% from 2019, when we had just $185. I suppose I have been putting a decent effort into building a taxable income stream from my MOB REIT portfolio.

We currently own three healthcare REITs in our taxable brokerage account. These REITs mostly give me exposure to the relatively stable medical office building space. Between the three REITs, this is how the dividends came in in 2020.

- Global Medical REIT = $637.20

- Physician Reality Trust = $624.14

- Welltower Inc = $276.94

$637.20 + $624.14 + $276.94 = $1,539.28

Here are all of the fourth-quarter dividends that hit my Fidelity account in late 2020.

Non-Dividend Distributions

I find non-dividend distributions interesting. The real estate investment trust is returning part of my original investment back to me. In other words, they don’t issue these payments from the corporation’s earnings or profits. These distributions reduce my cost basis in the REIT and the IRS won’t tax me until I sell the position.

Just over 39% of the $1,539 in REIT dividends I received in 2020 were considered non-dividend distributions. This total came in at $606. In other words, 39% of the cash flow generated from this investment will not be taxed in 2020.

When I do sell the position, we will pay the capital gain tax rate. But in the meantime, I can reinvest the cash. The $606 distribution represents about 52% of the dividends I received from GMRE and DOC. I did not receive any non-dividend distributions from Welltower in 2020.

Section 199A Dividends

If you recall from my 2019 experiment, a good chunk of this income is considered Section 199A Dividends. In our case, $824 of this income falls into this category. These dividends are treated very much like non-qualified dividends and are taxed like regular income from my W2 job. That said, they don’t get hit with FICA taxes like my regular income.

Here is the total:

Since Mrs. Max OOP is not working much these days, that keeps our income nice and low. So these dividends landed nicely square in the 22% tax bucket.

One thing that is nice about my Section 199A Dividends is they come with a special qualified business income deduction.

Qualified Business Income Deduction

Just like any other tax deduction, the qualified business income (QBI) deduction reduces our taxable income. The calculation on this is simple. We simply take my Section 199A Dividends and multiply them by 20%.

$824 X 20% = $165 QBI tax deduction

This deduction allows me to deduct $165 from our income and excludes that from taxes leaving $659 taxed at the 22% tax rate. That brings us closer to 17.5% tax rate on this portion of the dividend.

$659 X 22% = $145 Tax

Long Term Capital Gains

Last, we classify a portion of Welltower’s dividend distribution as a long-term capital gain. This total came in at $108.81, and it will be taxed at the long-term capital gain rate. In 2020 this was 15% for the Max Out of Pocket crew.

$108.81 X 15% = $16.32

Final Summary

Here is a summary of how our 2020 taxable REIT dividend income breaks down:

- Non-dividend distributions = $606 (taxed at 0% in 2020)

- Section 199A dividends = $824 (taxed at 22% after QBI deduction)

- Long term capital gains = $109 (taxed at 15%)

- Total = $1,539

The 2020 taxes on this income came in at $161, which equates to about 10.5%. Of course, we will need to plan for future capital gains taxes on those non-dividend distributions. I am okay with that, and I think there is some strategy there.

Cashflow-wise, that leaves us with $1,378. Again, not bad for a little side hobby.

Final Thoughts

It is amazing what you can do with your extra capital when you live a reasonable standard of living. After taxes, this $1,378 in income would cover about 3% of our 2020 annual spending, and this is just a small piece of our portfolio. Could I have made more money elsewhere? Of course. But I like boring.

I should also mention, this REIT income above was included in our total 2020 investment income summary from several weeks back.

I am sure some will wonder why I go through the effort of building this MOB portfolio. Why not invest it into the total stock market index like the rest of my portfolio? There are three answers:

The first and most important is education. I am trying to educate myself on how taxes and REIT dividends work. When I started this two years ago, I had no idea non-dividend distributions existed. I also did not know about the qualified business income deduction. Some of the tax advantages here have been a pleasant surprise.

Secondly, I consider this speculative investment that is a separate and distinct strategy from the total stock market index. I am not trying to beat the total stock market index with it, and I am just trying to build a dependable income stream that I understand and is diversified from the total stock market index that is currently sitting at an all-time high.

Finally, I just needed a another hobby.

We are not financial/investment or healthcare professionals and have no formal training. Always seek out a professional for financial advice and a trained healthcare provider for healthcare advice. This site and author are NOT responsible for any losses or damages you may incur in your own investing. Always consult with a certified professional before making any financial decisions.

Max

The post 2020 Taxable Healthcare REIT Dividends appeared first on Max Out of Pocket.

]]>The post What Ever Happened To Max’s Medical Office Building Portfolio? appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

My original idea was cute. Max from Max Out of Pocket would build a portfolio of medical office building REITs that would be structured in such a way that it could pay down his annual max out-of-pocket ($6,600) every single year from passive dividend income. A form of “healthcare independence” paid for directly by the industry. An industry that almost burned me out.

Max would go down as a hero who finally beat the system.

But then this thing called COVID-19 showed up and the industry got hit. Hard.

My investments did fine, but clinical folks have been stretched to the brink. Hospital systems and other healthcare companies around the country have been mobilizing a response to the pandemic. It has been unlike anything we have ever seen, and pretty amazing. That’s what we should be talking about, not investments.

I also had the realization that the industry didn’t burn me out, I burned myself out. That’s on me. These days, I am really enjoying my work and the contributions I make to the healthcare industry. That includes this blog.

All that said, I do not like leaving things open-ended. So, I wanted to go ahead and provide an update of where things stand with my MOB portfolio and where we will be going from here. I find writing about this stuff promotes action, and action produces results. The goal of this series was to learn a few things, and we did just that. Hopefully, that can continue.

With that, not only am I pumping the brakes on the project for 2021, I will be simplifying things a bit.

Max Almost Made It

I still think this was a good idea.

In fact, I almost made it. As of 12/12/2020, the $75,000+ portfolio was projected to generate almost $4,000 in dividends during 2021.

We could already easily cover my $3,300 family deductible with dividends from these investments. Every single year.

We are only $2,600 away from being able to completely cover our $6,600 annual max out-of-pocket.

But we are going to have to leave it there, at least for now.

The truth is, Max’s guilty conscience is not behind this decision to slow things down. Even with everything going on, we still need someone to invest in these buildings and provide a place for patients to receive care. That’s just the way the world works right now. And I really do not have any problem if that investment activity happens to generate a few dollars of income. In many respects, these investments support the healthcare industry.

But now is not the time for a victory lap.

Max Simplifies His Personal Finance Life

The main reason I am putting things on pause is for my own personal agenda. Simplicity and finesse. I have been making a deliberate effort to simplify our personal finance life ahead of 2021. This includes consolidating accounts and cleaning up target allocations. I am even creating an investor policy statement to keep me in line. By the end of the day, a five-year-old will be able to manage our finances.

Having a medical office building REIT portfolio spread out over three different accounts is somewhat inconvenient. So, we will be looking to streamline that, while keeping the heart of the portfolio intact in our taxable brokerage account. Additionally, as I firm up my investor policy statement, it’s starting to look like having $75,000+ of my liquid portfolio tied up in medical office buildings will be a bit much. That is, at least in the short term.

I should also mention that I have lost some interest in the project. I am learning that I only have so much capacity for it. Keeping track of individual stocks can be a challenge considering everything else I want to be focusing on.

This is something I was aware of when I bought my first medical office building, but it has become even more evident in 2020. Ultimately, my interest in other things is starting to take priority.

Portfolio Status

So where do things stand? The portfolio is up over $13,000 since I started.

Let’s start with the lesson of consistency. Like clockwork, I have stayed committed to dollar-cost averaging into this portfolio every two weeks. I have contributed every payday for over 18 months. Sometimes, I did it on my lunch break.

However, back in July, I decreased those investments to $500 increments as I started to focus on other things. That included funding both a 50k emergency fund and a 100k opportunity fund. Back in March, I quietly added a third REIT to the holdings called Welltower. It has done nicely since I purchased it and is up almost $2,500 as of 12/12/2020. No, I didn’t buy it just because I liked the name of the company. Though, “Welltower” does have a nice ring to it.

Our Risky and Speculative Investments

At the time of writing this, the portfolio has grown to over $78,670 and is spread out across three different accounts. I categorize this investment as a portion of the “speculative/alternative” allocation of our portfolio. You know, things like Bitcoin and marijuana stocks. But I happen to consider the purchase of any individual stock speculative. That allocation is required to remain less than 10% of our total assets.

In other words, these REITs are part of my “fun” investments.

Where do I keep these medical office buildings? This is how things are currently split up.

- Liquid Brokerage ($40,407)

- Traditional IRA ($28,444)

- Roth IRA ($9,819)

Having this in three different accounts has become a problem. Although a minor problem, it is something I am looking to simplify by eliminating the positions in the two red accounts.

Return on Investment

As of 12/12/2020, between dividend and capital gains, this project has netted $13,660 over the last two years. That is a 19.54% return on my original investment of $69,913.

Not bad considering almost half of that was invested in the last year alone. That is more than enough to put a roof over my head for an ENTIRE year.

Exactly $4,903 of that came through passive dividend income, and the rest is holding as an $8,757 unrealized capital gain on paper.

Here is a brief history of the dividend payouts. I sometimes refer to these as my rent checks:

- 2018 Q2 = $88.78

- 2018 Q3 = $152.72

- 2018 Q4 = $197.80

- 2019 Q1 = $197.80 (blog starts)

- 2019 Q2 = $197.80

- 2019 Q3 = $314.41

- 2019 Q4 = $455.86

- 2020 Q1 = $578.46

- 2020 Q2 = $843.35

- 2020 Q3 = $915.62

- 2020 Q4 = $960.70

- Total = $4,903.68

Man! And things were just starting to pick up steam!

Like I mentioned, the MOB portfolio is projected to generate another $4,000 in dividend income in 2021. That would cover almost 8% of our entire 2019 spending of $51,436 without lifting a finger. And we will spend less than $50,000 in 2020.

$4,000 / $51,436 = 7.8%

Time to Reorganize

However, the time has come to reorganize the portfolio. I was initially trying to demonstrate the difference between taxable accounts, tax-exempt accounts, and tax-deferred accounts. That exercise put individual REIT stocks in my retirement accounts. For me, having individual stocks in my retirement accounts is not the best practice. Therefore, it is something I have decided to move away from. I generally reserve those accounts for index funds only.

So, I have opted to move the entire portfolio into our taxable brokerage account. With that, I will reduce the balance back down to about $50,000. I still remember when the portfolio hit $50,000 for the first time.

The revised goal is to generate about $3,300 per year ($275/month on average) in taxable dividend income which will cover my 2021 annual family deductible.

I will then let this portfolio percolate for all 2021.

I will also likely stop regular dollar-cost averaging contributions for 2021 to focus on correcting my portfolio’s overall target allocation. That said, I do reserve the right to make lump sums contributions as the market fluctuates, assuming I stay within target allocations dictated by my investor policy statement. We will get to that another day.

Brokerage Account

Here is the balance in my brokerage account as of 12/12/2020. This is where the entire portfolio will ultimately land.

This comes up to just over $40,000 and is where a majority of the portfolio lives. As is, we are projecting annual taxable dividend payments out of this account to come in at $1,973 in 2021. This income will all be taxable, and I have a solid understanding of how that works.

- DOC : 971 shares X $0.92 annual dividend = $893.32

- GMRE: 820 shares X $0.80 annual dividend = $656.00

- WELL: 174 shares X $2.44 annual dividend = $424.56

$893.32 + $656 + $424.56 = $1,973.88 projected 2021 income

We are currently showing an unrealized total capital gain of $5,924 which will all be considered long-term capital gains in 2021. That could be something I look to harvest in 2021 at a lower tax rate.

Roth IRA

As for consolidation and selling off assets, I will start with our Roth IRA account since that is the smallest position outside of my brokerage account.

As I write this, that balance sits at $9,819.20 and shows a total gain of $890.61. That does not include the dividends that paid out since establishing the position. The only MOB investment in this account is Physicians Realty Trust. I know exactly how they make me money.

I will start selling off these investments in December 2020 and attempt to close out the position by the end of the year. I will dollar-cost out of this investment over the next few weeks and make offsetting purchases in my brokerage account until I get back up to $3,300 in annual dividend income.

Since this is a Roth IRA, I will never be taxed on that $800+ capital gain or any of the dividends already received.

Traditional IRA

This position might take me a few months to simplify. It holds $28,444 and is spread out over two positions of DOC and GMRE. These will be slowly sold off and replaced by some form of the total stock market through an index fund.

Since this is a traditional IRA, these capital gains and any dividends already received will not be taxed until I withdraw the funds at traditional retirement age several decades from now.

Final Thoughts

It was evident when I started this blog that I needed a hobby. In addition to the blog-writing itself, the MOB portfolio has undoubtedly been an interesting hobby for me. At $13,000, it probably pays more than selling (insert shitty product here) to my friends and family. Hopefully, less annoying, too.

But the time has come to simplify things.

I am not pulling the plug on the medical office building portfolio altogether, but we will be downsizing a bit. When all is said and done, the entire balance will live in our brokerage account and hopefully generate about $3,300 in passive “rental” income. Things should be much easier to keep track of as we move forward.

This transition does not need to happen overnight. The goal of this post is to prompt action and get things moving in the right direction. I think this will happen over the rest of 2020 and even as we move into 2021. I will post an update when this is complete.

Basically, my goal here is to get all “alternative/speculative” investments out of my retirement accounts. They really do not have a place there and it goes against my overall strategy. Above all, I am going for automation, simplicity, and systemness (I like that word).

Finally, I do like the idea of being able to earmark these dividends for my deductible. It is a good feeling that stays within the parameters of my original vision.

What do you think about individual REITs? Is Max taking crazy pills?

The post What Ever Happened To Max’s Medical Office Building Portfolio? appeared first on Max Out of Pocket.

]]>The post Tax Treatment Of My REIT Dividends Part 2: Non-Dividend Distributions appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

So, I took a long hard look at how my medical office building REIT dividends are taxed. To accomplish this, I purposely generated about $100 in dividend income from my stake in Physicians Realty Trust (DOC). This hundred bucks hit my brokerage account in mid-October of 2019. Up until then, I was following the herd and keeping most of these assets in my retirement accounts so I wouldn’t need to worry about taxes.

435 shares X $0.23 dividend per share = $100.05

Non-Qualified Dividends

As you might remember, we already know I paid about $8.00 of this to the federal government for the $44 non-qualified portion of the dividend.

Through that exercise, we found out that the non-qualified dividends paid out from my healthcare REITs are taxed just like regular income. That’s not ideal. We call non-qualified REIT dividends “Section 199A” dividends. They hit my regular tax bucket just like all my other regular income does. For Mrs. Max OOP and I, that comes out to about 22 cents on the dollar. That’s because we land in the 22% tax bucket. For tax purposes, we would much rather see qualified dividends because they are taxed at the more favorable long-term capital gains rate of 15%. That’s a 7% spread and comes out to $70.00 for every $1,000 in taxable income.

As it turned out, only about $44.00 of the $100 was considered non-qualified dividends. I even got a deduction to lower the $44.00 in taxable income even more. At the end of the day, I only paid $8.00 in tax on my $44.00 non-qualified dividends. That came in at 8%.

But what about the other $56 in non-dividend distributions?

Non-dividend Distributions

Here is a look at my non-dividend distributions directly from my tax form:

The $56 distribution represents the “return of capital”. In theory, I am getting some of my original investment back. The non-dividend distribution is the depreciation deductions for the assets within the fund. In my case, the medical office buildings in the portfolio are depreciating and I get some of that back.*

The $56 did not hit my 2019 tax return and I was not taxed on it in 2019. The cash flow still hit my brokerage account, but I didn’t need to worry about the taxes.

I don’t get off scot-free, though. Eventually, a tax will be assessed. But not at the regular income tax rate.

How Does it Work?

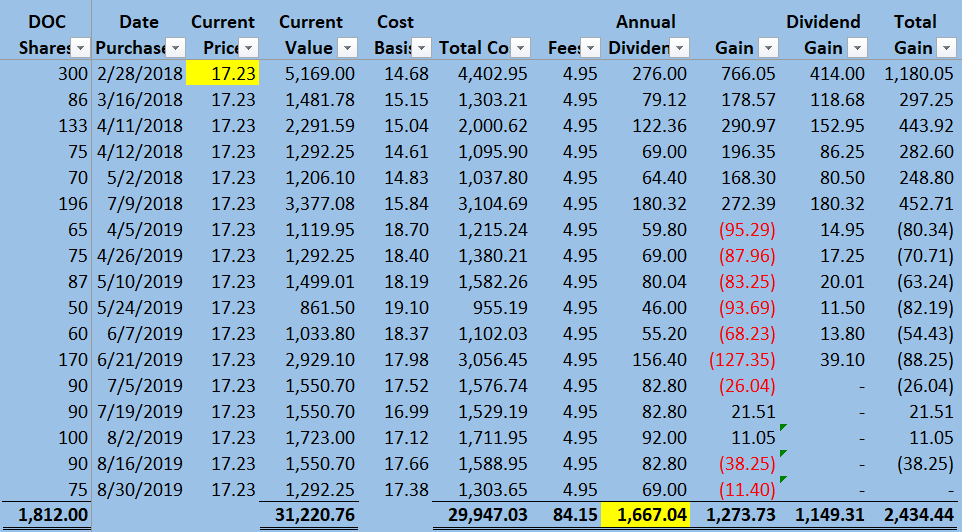

As I mentioned, I needed to buy 435 shares of Physicians Realty Trust from August to September 2019 in order to generate the $100 in income. These are the specific shares of the company that generated the $100 in total dividends referenced above.

As you can see, my total cost for actually purchasing these 435 shares was about $7,642. This is considered my “cost-basis” and it is used for figuring out capital gain taxes should I ever sell the stock. That tax rate is between 0%-20% for long-term capital gains. For most people reading this, it is probably 15%.

Cost Basis = $7,642

The average cost basis on these 435 shares was $17.57 when I bought them.

$7,642 / 435 = $17.57 = average cost basis per share

But let’s say the value of my 435 share investment grew by $100 to $7,742. This would put the share price of DOC at about $17.80. If I decided to sell at that price my capital gains would be $100, right?

435 X $17.80 = $7,742

$7,742 – $7,642 (cost basis) = $100 capital gain

Wrong again, Max.

Chopping Away My Cost Basis

Because I was returned $56 in capital from the 435 shares in Q4 2019, my cost basis was reduced by $56. It is no longer $7,642.

$7,642 – $56 = $7,586 = new cost basis

So my capital gain on the investment if I were to sell at $17.80 is actually $156.

$7,742 sale price – $7,586 new cost basis = $156 = capital gain

When I go to sell Physicians Realty Trust, I now have $156 gain to deal with; $100 price appreciation and $56 non-dividend distribution.

$100 (true capital appreciation) + $56 (non-dividend distribution) = $156

Don’t take my word for it, here is a look at the actual shares:

Here is another way for me to demonstrate the same concept. See how much I paid for those shares on 9/30/2019? From below, you can see the cost basis on the transaction was $3,037.75. But from above, you can see the non-dividend distribution related to those shares reduced my cost basis on the same set of shares to $3,015.81.

What Does All of This Even Mean?

Clearly, REIT taxation is a complicated topic. However, so far I am not as scared of the income as I once never was. In theory, a 15% long-term capital gain tax will eventually hit my $56 non-dividend distribution.

$56 X 15% = $8 capital gains tax

I was already taxed $8 in 2019 on my $44 nonqualified dividends. Now I am looking at another $8 tax on my future capital gain on the $56. We are up to a $16 tax on my $100 dividend.

$16 / $100 = 16% tax rate

As you can see, the non-qualified dividend tax and the future capital gain tax will come in at about $16, for a total of about 16%. This is much lower than the 22% I was thinking.

Final Thoughts

In short, the taxes on my non-dividend distributions are deferred until I sell the investment. They will be taxed at the long-term capital gain rate the year I sell the shares. For those of you out there interested in early retirement, I am starting to see a little strategy here, but we will have to cover that another time.

This got me wondering if there is a misconception about REITs. Are people just taking the easy way out and throwing them in their tax-advantaged accounts so they don’t have to worry about the tax details? For me, a 16% tax rate on my passive income seems reasonable. I don’t even have to pay Medicare FICA or Social Security FICA on it.

REIT taxes are tricky, so I will leave it at that so you can read through it a few times. I wrote this and even I had to read it a few times. In the meantime, I am planning on growing my brokerage REIT allocation as we move through 2020 so we can run through this calculation again in 2021 with some bigger numbers.

*If anyone has additional commentary on this, I would love to hear it in the comments.

Usual disclaimer, I am not a tax professional and this is not tax or investment advice. It is not a recommendation to buy anything and you are responsible for your investing decisions.

Just like the IRS does, I rounded the numbers above to the nearest dollar. For fun, I did the same calculation out to the decimal and came up with a total tax rate of 16.14%

The powers that be could always change the 0% – 20% long term capital gain tax rate. So just like any other responsible investor, I will keep an eye on those regulations.

The post Tax Treatment Of My REIT Dividends Part 2: Non-Dividend Distributions appeared first on Max Out of Pocket.

]]>The post Tax Treatment Of My REIT Dividends Part 1 appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

But Max strictly follows the policy of ‘trust but verify’. So I purposely generated $100 in taxable REIT dividend income in my brokerage account in 2019. That way, I could follow it through to my tax return and see how much the IRS pulled out of my pocket.

I used part of my medical office building portfolio to make that happen. As I have said from the beginning, we need to learn a few things from this experiment. I am willing to complicate my life a bit in an effort to understand how things work.

Don’t say I didn’t give you fair warning, though. This write up is full of tax terms and numbers. You can handle it.

My Healthcare REIT Income

Between August and September of 2019, I purchased 435 shares of Physicians Realty Trust (DOC) in my taxable brokerage account.

The goal here was to generate about $100 in 2019 REIT dividend income for me to play with. DOC was generally paying a $0.23 per quarter dividend on each share. The plan was for this income to hit in the fourth quarter of 2019. Sure enough, in October of 2019 Physicians Realty Trust paid me $100 in dividends. Those dividends hit my brokerage account.

435 X $0.23 = $100

Let’s follow this $100 through my tax return. As we already know, the Max Out of Pocket crew lands solidly in the 22% tax bucket. This is my marginal tax bracket. I call these buckets, not brackets. In fact, I busted tax brackets awhile back. For every dollar I add to my 22% bucket, 22 cents goes to the taxman.

REITs usually throw off ordinary dividends that are not “qualified”. Qualified dividends get special tax treatment since they are taxed at the long-term capital gains rate of either 0%, 15%, or 20%. Nonqualified dividends, on the other hand, get taxed at the ordinary income tax rate. So the theory was adding nonqualified ordinary income to my 22% marginal tax bucket should cost me about 22 cents for each dollar of income my REIT generates. I was thinking it would look something like this.

$100 Nonqualified REIT Income X 22% Marginal Tax = $22.00 Tax

But I wanted to test this. Would the IRS really take $22 from my $100 in hard-earned REIT money? As it turns out, there are several other moving parts to this.

Ordinary Nonqualified Dividends

To my surprise, only 44% of this $100 in dividend income was considered ordinary nonqualified dividends. They are technically called “Section 199A” dividends but I am just going to call them nonqualified dividends from here on out. Apparently, companies like DOC release this information annually and it looks something like this.

44% X $100 REIT Income = $44.00 Ordinary Nonqualified Dividend

As I said above, I prefer dividends that are considered “qualified” dividends so we can pay the lower capital gains tax rate on them. That is one of the so-called drawbacks of REITs. Since this $44 in dividends is considered nonqualified, it hits the ordinary tax bucket just like all our other earned income does. In other words, it is taxed just like income I generate from my employer by trading my time for money. This is how it looked on my 1099-DIV tax form:

Most of the remaining part of the dividend was considered a non-dividend distribution. And just like that, we have a new term to learn.

Nondividend Distributions

The rest of my $100 dividend was a non-dividend distribution. This came out to about $56. I am going to cover this in more detail in part 2 of this post, but this portion technically didn’t even hit my 2019 income tax return and I was not taxed on it in 2019. I will need to worry about this in the future, but the take-home here is the $56 was not taxed in 2019. This concept blew me away. There is also a very small capital gain distribution that is completely immaterial on a $100 dividend so I won’t bother covering that today.

56% X $100 REIT Income = $56 Nondividend Distributions

So does this mean only the $44.00 in non-qualified ordinary dividends gets taxed at 22% in 2019? Yes and no.

To The Tax Return

So for tax purposes, this $44.00 in ordinary nonqualified dividends is all I needed to worry about in 2019. It landed on line 3b of my tax return (Ordinary Dividends). Since they are not “qualified” dividends, they are not reported on line 3a (Qualified Dividends). I realize I am being redundant, but I need to drive this concept home.

The $44.00 travels down the tax return to my total income on line 7b (total income) and eventually down to 8b (adjusted gross income). I assumed at this point, it would be taxed something like this.

$44.00 X 22% = $10 Tax

Wrong again, Max.

The Unexpected Qualified Business Income Deduction

Apparently, owning a healthcare REIT like DOC made me eligible for Qualified Business Income Deduction. This deduction is backed out of my income before the income tax is applied. It is a similar concept to the standard deduction. The calculation is pretty simple. For me, they took my total nonqualified REIT dividend income and multiplied it by 20%. It was easy for me, but there are a few other moving parts to this depending on the situation.

$44.00 X 20% = $9.00 Deduction

This $9.00 deduction lands on line 10 of my 1040 Tax Return. In theory, it reduces my $44.00 in non-qualified dividends by another $9.00 for tax purposes.

That leaves me with $35.00 in taxable income

$35.00 X 22% Marginal Tax Rate = $8.00 Tax

That tax on my $44.00 dividend is roughly 18%.

$8.00 / $44.00 = 18% Tax Rate

Take-Home

Evidently, humans like to make things complicated. This complexity probably keeps more than a few people employed. But at the end of the day, it’s good news for me. The IRS pulled $8.00 out of my pocket for income taxes on the $100 in dividends I received from DOC in 2019. We still have some homework to do on that $56 in non-dividend distribution. But so far I am feeling pretty good about this $8.00. This comes out to only 8% on the $100 I received. Perhaps I need to consider increasing my brokerage allocation.

$8.00 / $100 = 8% Tax

This is all thanks to the non-dividend distribution and the unexpected qualified business income deduction.

This $8.00 tax is pretty reasonable if you ask me. But what about those non-dividend distributions? Perhaps we have an opportunity to use a sabbatical or early retirement to time the release of the non-dividend distributions for tax purposes? More on that next time, here at Max Out of Pocket.

Interested in Part 2? Check it out here to see how those non-dividend distributions are handled here.

Max is not a CPA and this is not tax advice. It also isn’t a recommendation to buy REITs or any other investment. As always, you are responsible for your own investing decisions. That said, if a real-life accountant wants to validate any of my findings, please do so in the comments below.

Just like the IRS does, I lightly rounded the numbers above to the nearest dollar.

The post Tax Treatment Of My REIT Dividends Part 1 appeared first on Max Out of Pocket.

]]>The post My $50,000 Medical Office Building REIT Portfolio appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

I will go ahead and call this an accomplishment. This 50k healthcare REIT portfolio is worth quite a bit more than the annual salary I received for my first job out of college. $50,000 might be a drop in the bucket for some people, but it took me a long time to get here. To date, I have realized over $2,100 in passive dividends from it and it is projected to throw off another $2,500 in dividends over the next 12 months. I sometimes refer to this as my “rental income”.

But Max isn’t naive. I know there are plenty of other investments out there. With its 30%+ monster gain, a simple S&P index fund on its own would have beat my MOB portfolio outright in 2019. But I am happy where things are and I have learned a ton about REITs.

We all know that deep down Max is a total stock market index fund investor with little interest in picking individual stocks. I was lucky enough to start my career at the beginning of an unrelentless bull market where I couldn’t lose on index fund investing if I tried. But these days, I am making some exceptions. I suppose everyone needs a hobby. With a new milestone reached here at Max Out of Pocket, I thought a little update on the portfolio wouldn’t hurt.

Where Do I Keep My Medical Office Buildings?

We covered this in-depth here, but it is worth a brief update. The Max Out of Pocket medical office REIT portfolio is split across three very different accounts; Brokerage, Roth IRA, and Traditional IRA. These three accounts all handle taxes very differently. Since REITs tend to throw off a lot of dividends, it is important to understand how each of these accounts handles the taxes on those dividends. This little experiment has proven to be a nice case study on how each of these accounts works.

Here is a look at the balance in each of my accounts.

My favorite account for this type of investment is the Roth IRA. The Roth IRA offers tax-free growth and tax-free withdrawals during retirement. The dividends that hit this account from my medical office building portfolio will never be taxed.

My second favorite account is the traditional IRA. This account offers tax-deferred growth. This is where I hold the bulk of the Max Out of Pocket Healthcare REIT portfolio. The dividends that land in my Traditional IRA in 2020 will not have a tax applied to them in 2020. I can reinvest those dividends into other investments within the traditional IRA account. There is a catch, though. The tax is “deferred” on these gains until I withdraw the assets at retirement age. The tax rate depends on what tax bucket I am in at the time I start withdrawing from the account.

Coming in last place is my brokerage account. Dividends that hit this account in 2020 will be taxed when I file my 2020 return. As of today, I am projecting $863 in dividends will hit this account in 2020. Many people advise against holding REITs in a brokerage account. That’s because they throw off non-qualified dividends that are taxed like regular income. There is a flip side, though. Assets in this account are easy to access and I could easily sell all my medical office buildings REITs in this account tomorrow and have the 16k in cash within a few days. It isn’t that easy with the tax-advantaged accounts. Sometimes Max is willing to pay a premium for this kind of liquidity. Several of my investment transactions since August occurred in this account because I had easy access to fresh capital from my W2 job.

Diversification

I currently only hold two REITS in my medical office building portfolio. We started this experiment with Physicians Realty Trust (DOC) and later added Global Medical REIT (GMRE). So Max is breaking one of the cardinal rules of investing. Always diversify. Two REITs is not diversification.

I made the case for diversification several months ago when I decided to add GMRE to the mix. Although that helped, I still only own two stocks and could easily get burned by either one of these companies. I saw this earlier in 2019 when Physicians Realty Trust had some tenant issues down in Texas. Thankfully, my management team was able to work through it. If I continue to grow this portfolio, I will eventually need to consider additional healthcare REITS to help us mitigate risk specific to each of these companies. As of now, I am not too concerned about it since this MOB portfolio only represents a small portion of my overall portfolio.

All that said, we do have some geographic diversity built into these two REITs.

These maps show that between DOC and GMRE, my medical office buildings are pretty diversified throughout the country. They have a similar, but different, footprint. Should help us in a natural disaster situation. I hate black swans.

There is also no overlap with these two REITs’ top ten tenants. Another good indicator that these two investments are diversified from each other. DOC’s top tenant is CommonSpirit Health representing 20.1% of the total annualized base rent for the company. GMRE’s top tenant is Encompass Health representing 10.9% of the annual base rent. I recently sat by someone at a conference who worked at Encompass and she liked working there. I suppose that is my only technical look into the state of things over at Encompass so far.

Types Of Buildings

So what kind of buildings do I own through these REITs?

One of the things that got me interested in Physicians Realty Trust from the beginning is that their core portfolio is medical office buildings. About 93% of DOC’s portfolio is MOBs. Medicare and other payers are doing all they can to drive patients away from the expensive inpatient hospital setting. They want procedures done on an outpatient basis. DOC’s property acquisition strategy fits well into this trend.

GMRE has 55% of its portfolio in medical office buildings. But they also get me some exposure to the inpatient rehab facility (IRF) market. This represents about 28% of GMRE’s portfolio. These facilities have a pretty favorable reimbursement model setup with the Medicare program. The service they provide is very specific and space for rehab services is always going to be needed for obvious reasons. GMRE also has almost 10% of its portfolio in acute/surgical hospitals. So we get some overlap in the MOB asset class while also getting some exposure to other types of buildings.

Metrics

There are just a few metrics I want to point out and we can call it a day. Fund from operations (FFO) and dividend yield. I have covered both of these here.

DOC’s third-quarter conference call indicated a normalized FFO of $0.27 cents per share. Since they are currently paying a dividend of $0.23 per quarter, DOC seems to have the dividend solidly covered.

At current valuations, DOC’s dividend is yielding 4.79% annually. This is a pretty low yield compared to what I was getting on my purchases earlier in 2019. My overall yield on cost for the entire portfolio is about 5.69%.

GMRE’s third-quarter conference call indicated an adjusted FFO of $0.19 per share. The board declared a dividend of $0.20 that quarter, so the FFO is not completely covering the dividend. I am watching this closely, but since GMRE is in a growth phase I am not too worried about it.

At current valuations, GMRE’s dividend is yielding 5.41% annually. GMRE is generally a higher risk investment than DOC and part of the reason for the higher yield. But as one of the few REITs with 100% occupancy, in my eyes, they are offsetting some of this risk with performance.

Short Note On Fidelity Commission Fees

There are no more commission/transaction fees at Fidelity!

Max was pleasantly surprised to find out that Fidelity completely eliminated the $4.95 commission/transaction fee for online trading back in October. Yes, it’s true. After several of Fidelity’s competitors made similar moves, Fidelity really had no choice but to match the rest of the industry. So the Max Out of Pocket Healthcare REIT portfolio reaps the benefits of a super competitive brokerage industry with lower transaction costs.

I missed this news initially. But it just so happens my very last purchase of DOC on 9/27/2019 also marked the very last commission fee for my little REIT portfolio. Almost poetic. So the total cost to build this $50,000 portfolio was $89.10. This represents the $4.95 charge for the first 18 transactions of the portfolio. Going forward fees will be $0.00. Perhaps I should consider moving my dollar-cost averaging strategy up to weekly now that there is no more fee.

So Where Do We Go From Here?

Over the next 10 years, I should net about $25,000 from this portfolio in dividend returns. This assumes no capital appreciation or dividend increases. But where do we go from here?

There are really two options. I call this project done and allocate all future investments into the total stock market or bond index. This would include the $578 in quarterly dividends I am expecting to receive from this portfolio. That is the boring and probably safer option.

But I think we all know the more entertaining option is to take this portfolio to $100,000.

So I am probably going to keep this little project going. I still like medical office buildings as a long-term ten-year investment, and I have been enjoying my new hobby. So I will keep researching and learning as much as I can about healthcare REITS and hopefully start digging into a few other companies.

That said, my two REIT’s stock prices are up quite a bit recently. So I may or may not tone down the frequency of this investment while I research other options. I am still considering this part of my “speculative” allocation in my overall asset allocation and we do not want to put my overall portfolio off balance by sinking too much into this project.

As of today, I am not looking at a sabbatical or break from work in 2020. So I will have plenty of free W2 cash flow to continue to dedicate to this little project.

My next milestone will be a $100,000 medical office building portfolio. If I make it to the $100,000 mark, I will be able to pay most of my insurance’s max out-of-pocket in any given year with the dividends the portfolio generates. In the event of a medical issue, having a portfolio specifically earmarked for future medical expenses will make sure we can focus on getting healthy and not worrying about out-of-pocket costs. The 2020 Medicare Part A deductible passed $1,400 this year and it seems like keeping the program “premium-free” is unsustainable. Planning for these costs is a must.

Max could be wrong about all of this, though. So if someday we end up with Medicare For All with no out-of-pocket costs, I am going to buy myself a really nice vehicle with the proceeds from this portfolio.

This is not and never will be a recommendation to invest in this or any other type of investment. See my disclaimer page if you have any questions. You are responsible for your own investment decisions.

The post My $50,000 Medical Office Building REIT Portfolio appeared first on Max Out of Pocket.

]]>The post Why Global Medical REIT Inc? appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

That’s not to say I haven’t been busy behind the scenes dollar-cost averaging into my new favorite healthcare REIT. Since then, I have purchased over 300 shares of Global Medical REIT Inc. The total value of the Max Out of Pocket REIT portfolio is just over $43,000 and set to pay out over $2,000 in dividends over the next year.

Well, there was a pretty significant price run-up on Global Medical REIT Inc. (GMRE) since I made that case for diversification. I paid $11.85 for that initial position and the stock price increased all the way up to $14.13 by market closing 12/10/2019. That is a 20% gain in just over a month. We call that accidental timing. Max is good, but not that good.

Common Stock Offering – Dilution

That price run-up all ended for GMRE last week when we saw a 7.9% stock price reduction in one day.

Global Medical REIT decided to do an upsized offering of common stock to the tune of 6 million shares at a price of $13 per share. The gross proceeds from this offering were about $78 million. That event diluted my ownership in the company because new shares were issued, reducing the value of the shares I have been accumulating.

Since this is a long-term investment for the Max Out of Pocket medical office building portfolio, I am really not too concerned with this event. If anything, I am happy with the timing because they were able to raise a decent chunk of capital at elevated stock prices. It also might give me a chance to lock in more shares with a higher yield going forward.

But the real question is do I trust my management team to deploy that $78 million in capital strategically to make me money in the long run. Their relatively short history suggests they will.

Capitalization Rates

Before we dig too much more into GMRE, we get to learn something new today at Max Out of Pocket. Capitalization rates. We can call them “cap rates” for short. The cap rate metric helps us analyze and determine the potential annual rate of return for a particular property in a REIT portfolio.

So let’s formally define the cap rate. Generally, the cap rate for a property a REIT owns is the net operating income of a particular property divided by the current market value of that property.

CAP Rate = Net Operating Income / Current Market Value

Net operating income (NOI) is a little different than regular income. It is a before-tax figure that excludes interest payments on loans, capital expenditures, depreciation, and amortization. We could spend some time on NOI, but I am going to leave it at that.

The current market value is the amount of money the property might sell for in the open market today.

Divide these two and we have our cap rate.

Global Medical REIT Inc Q3 Conference Call

I listened in on several of GMRE’s conference calls before I officially became an investor with the company. My first earning conference call as an actual investor occurred 11/7/2019 for the quarter ending 9/30/2019.

GMRE is a much smaller company than my portfolio’s core position, Physicians Realty Trust (DOC). But the company has been staying very busy growing. They acquired seven properties in the third quarter of 2019 alone. These properties had an average weighted cap rate of 7.7%. These are higher cap rates than we are seeing over at DOC where they were running between 5-6% on Q3 purchases. The total purchase price for the properties GMRE purchased was about 66.1 million dollars.

One of those properties was in Livonia, Michigan and tied into Mission Health. That building cost $10.5 million and has a cap rate of 8.1%. This happens to be a market Max is relatively familiar with. The NOI/base rent is $855,000 per year.

$855,000 (NOI) / $10,500,000 (Market Value) = 8.1% Cap Rate

Through the Q& A, the management team made it very clear they are aiming to stay in that mid 7% cap range for the foreseeable future.

In other words, GRME is in a growth phase. With the $78 million stock offering referenced above, they could potentially acquire seven more buildings with similar cap rates. This could continue to grow the income stream and increase funds from operations (FFO). According to the press release mentioned above, the management team plans to use the $78 million in proceeds from the stock offering to repay a portion of outstanding indebtedness, fund acquisitions, and for other general corporate purposes.

GMRE’s Medical Office Building Portfolio

As of 9/30/2019, GMRE has 101 buildings with a total of 84 different tenants. They are one of the few healthcare REITs that are 100% leased. Their asset portfolio has grown from $124.8 million to $830.4 million as of 9/30/2019.

There are several things that make GRME different than DOC, but one of the key differentiators is that medical office buildings only represent 55.4% of their portfolio. Inpatient rehab facilities (IRF) make up 28% of their portfolio and Encompass (who is a decent player in IRF) is their largest tenant making up 10.9% of their annual base rent.

This gets the Max Out of Pocket healthcare REIT portfolio some exposure outside of the highly competitive MOB space.

Here is a look at their asset types:

Out of 131 leases, GMRE only has 3 of them expiring in 2020 and only 6 expiring in 2021.

Sweet Spot

GMRE’s chief investment officer Alfonzo Leon mentioned the (current) sweet spot for their acquisitions is between about $7-14 million. Since they are a smaller REIT, these smaller purchases can still drive some material growth for the company.

I was also happy to hear Mr. Leon suggest that they were being very selective on inpatient investment opportunities. The traditional Medicare program is driving as much as they can to the outpatient setting. He said the lion’s share of opportunities on the inpatient side are rehab hospitals. Although inpatient rehab hospitals have been targets of some RAC audits (in my experience), the reimbursement model for Medicare is usually pretty favorable and it will be hard to drive patients out of that setting since it is so intensive.

Like I said, Encompass Health happens to be their top tenant (10.9% of the base monthly rent) and is a big player in inpatient rehab hospitals.

Final Thoughts

I am still learning my way around Global Medical REIT Inc, but I am certainly happy with the short-term results and long-term growth opportunity. GMRE is small, but with that comes mobility and the ability to strategically grow. It also brings risk, a risk I am willing to take for the higher short term yield on my investment.

At the time of writing this the dividend yield for GMRE is back over 6% where DOC is closer to 5%. We will eventually do a side-by-side comparison of DOC and GMRE to get a better idea of how these two REITS compare.

Do you own any medical office building REITS?

The post Why Global Medical REIT Inc? appeared first on Max Out of Pocket.

]]>The post Healthcare REITs: A Case For Diversification appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

The problem is all this growth has been surrounding purchases of one REIT: Physicians Realty Trust (DOC). As much as I like DOC, owning just one healthcare REIT has exposed this little chunk of my portfolio to unnecessary risk. With a few minor tweaks, we can slowly start mitigating some of this risk.

Since I got another $455.86 in dividends yesterday from DOC, perhaps now is a good time to start thinking about how we can use that money to employ a diversification strategy.

In other words, we are finally going to start tightening things up around here at Max Out of Pocket.

If you need to catch up, you can find all my notes on this project here.

Diversification

The technical definition of diversification, according to Vanguard, is:

The strategy of investing in different asset classes and among the securities of many issuers in an attempt to lower overall investment risk.

Per Vanguard

Yikes, I am breaking both ends of the definition. My medical office building portfolio owns one asset class and one security made by one issuer. What a sucker.

On the surface, Physicians Realty Trust is technically pretty diversified. Our portfolio of medical office buildings is spread out over 30 states. No metropolitan statistical area (MSA) represents over 8% of leasable square footage. No single tenant is responsible for more than 6% of the annual base rental revenue coming into DOC. You can review a lot of this information on their September 2019 investor presentation slides.

Here is a nice map showing the location of all the medical office buildings (and a few hospitals) I own through DOC.

But at the end of the day, this is still only one company. By owning just one REIT stock in my medical office building portfolio, I am exposing myself to risks that are unique to this company. This is also known as “specific risk”.

This is one reason so many people in the FI/RE (Financial Independence / Retire Early) community purchase all the stocks in the stock market using a total stock market index fund. Their strategy eliminates specific risk by diversifying into thousands of companies across the entire stock market. I personally follow the same strategy for the majority of my overall investment portfolio.

Why I Started With One REIT

There was actually a method to the madness of selecting only one medical office building REIT stock. I wanted to completely break it down into bite-sized chunks. It made everything easier to digest and understand since I was far from an expert in healthcare REITs. I was able to evaluate specifically how Physicians Realty Trust makes me money and also get into quantitative metrics that I could monitor along the way. We learned a bit about conference calls, passive income, and dollar-cost averaging on my lunch break. Finally, we also found out where I am keeping all these medical office buildings to help me plan for taxes.

Pulling in other healthcare REITS into the mix prematurely would have been too much information to digest and could have potentially bogged down the experiment.

But as this little portfolio has matured and set goals, things change.

More On Specific Risk

Although DOC’s portfolio is relatively diversified throughout the United States, there is still risk specific and unique to this company. I like to use unexpected erratic behavior by a CEO as an example, but there are plenty of other examples.

Here are just a few of my favorite kinds of risk.

- Operational risks are the everyday risk of running a company. Think of them as unforeseen events, negligence, or straight-up fraud within the company. Even if I was the CEO of Physicians Realty Trust, I would have no way of knowing everything that is going on in the day-to-day operations. An IT data breach releasing customer information in error or an accounting mistake specific to the company could quickly derail financial performance. We actually saw some operational risk earlier this year when we had a tenant down in Texas stop paying rent.

- Strategic risks are the possibility of breakdowns in strategy. We already know how DOC makes me money, but what if that strategy was wrong? Let’s say Physicians Realty Trust was buying up malls instead of medical office buildings so they could rent those buildings to retail companies. Since so much is being handled online, there seems to be a correction going on in the mall market. That strategy could be suspect in 2019. We are already seeing some of this in the healthcare space with a push to telehealth. Will Walmart, CVS, or Amazon cut down on the need for medical office buildings? Maybe.

- Legal and regulatory risks can come from the government, customers, or even competing firms. If the Texas Medicaid program was to wake up one day and decide to cut reimbursement for services provided in a medical office building, we might have a problem. Physicians Realty Trust owns a lot of buildings in Texas, so this risk might adversely impact our financial performance.

So how do we help manage risk specific to Physicians Realty Trust? We buy another healthcare REIT.

Global Medical REIT Inc (GMRE)

The goal of this blog is usually educational in nature. Making money is great, but we already have enough money to fund a pretty fancy lifestyle. So when I look to pull another REIT into the equation, the goal is twofold:

- Give us another company in the industry to compare some of our Physicians Realty Trust metrics (like FFO and Revenue) so we can grow our understanding of healthcare REITs.

- Provide some light diversification to protect the Max Out of Pocket Healthcare portfolio from the specific risk associated with Physicians Realty Trust.

So in an effort to accomplish the goals listed above, I have expanded the Max Out of Pocket healthcare REIT portfolio into another company. On October 11th (payday), I purchased 110 shares of Global Medical REIT (GMRE) for $1,269.40. These shares will generate about $88 in passive income over the next year.

We won’t review too much of the company specs on this post, but it is a smaller company that is yielding an annual dividend of about 6.75% at the time of writing this. After sitting in on a few conference calls with the company, I like what I am hearing. We will go into much more detail on this investment in a later post.

As I mentioned above, yesterday I received $455.86 in passive dividend income from Physicians Realty Trust. I will use this income to buy about 40 more shares of GMRE on payday next week. See how that works? I am using the income from one healthcare REIT to buy into another healthcare REIT. Let the compounding growth process begin. These 40 shares alone will generate about $32 in passive income over the next year.

Final Thoughts

The time has come to start cheating on Physicians Realty Trust (DOC) in the name of diversification.

I’ve said it before, the Max Out of Pocket REIT portfolio is just a subset of my entire investment portfolio. So it isn’t like I have been investing my entire life savings into Physicians Realty Trust. That would be a recipe for disaster and a bit reckless. But at this point, it is worth implementing a diversification strategy. I am still working full time, so I don’t have the bandwidth to follow several stocks, but I think I can manage two. Here is a look at where we are with the portfolio.

My current plan is to grow my medical office building REIT portfolio to about $50,000 and have enough passive dividend income to cover the majority of my max out-of-pocket healthcare costs in any given year. But I can no longer justify having only one company in the portfolio. There is just too much specific risk that comes along with that. So at this point, I will plan on holding my position with Physicians Realty Trust (DOC) at 1,982 shares for the rest of 2019 and start to build up the portfolio in other areas. This growth will start with Global Medical REIT Inc (GMRE).

Do you own any medical office buildings?

Usual disclaimer: I am not an expert in REITs and this is not a recommendation to buy either of these stocks or any other stocks. You are responsible for your own investing decisions.

The post Healthcare REITs: A Case For Diversification appeared first on Max Out of Pocket.

]]>The post Healthcare REITs: Back To The Basics appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

Those of us in the early retirement/financial independence community like to do fun stuff in our free time like calculating our savings rate. We then take these savings and invest them in fancy-sounding things like the total stock market index. You may know the slogan – spend less, save more, invest the difference.

Saving Rate

A simple version of this calculation is our gross household wages minus household expenses divided by our gross household wages. Basically, the operating margin of the household for all you CPA’s out there who are much smarter than me. Pretty easy calculation once you do it a few times. If your household makes $100,000 per year and spends about $50,000, you have a rock-solid savings rate of 50%. Congratulations, invest that $50,000 savings and you are well on the way to early retirement. You can even buy medical office buildings if that strikes your fancy.

$100,000 Gross Wages – $50,000 Expenses = $50,000 Savings

$50,000 Savings / $100,000 Gross Wages = 50% Savings Rate

When someone like Max OOP starts looking at the quarterly financial statements of healthcare REITs like Physicians Realty Trust (DOC), it is a bit daunting. They are several pages long and have confusing sounding words and acronyms littered throughout the statements. My initial focus was to completely break these statements down, look for holes, and use it to help evaluate the investment.

But sometimes, we need to take a step back and look at the basics of business. I already know how Physicians Realty Trust makes me money, but that is just theory, strategy, and words on a blog. In the end, I really need more quantitative data to prove it. Just like monitoring a household savings rate, there are three very basic concepts and things to monitor when we own a REIT; Revenue, Expenses, and Income.

Total Revenue

Revenue is easy.

I like to compare healthcare REIT revenue to the Max Out of Pocket household’s paychecks from our day jobs. We both provide a service to two different companies, and the result of that service is our wage. If our household was a business (I basically run it like one), I could go as far as to call this our household revenue. The services we provide are diversified into two different fields; teaching math and counting healthcare beans (finance).

Healthcare REITs such as Physicians Realty Trust (DOC) offer a different kind of service. They deliver a physical space to provide healthcare services, usually on an outpatient basis. Providing and managing the physical space is their product/service, and the result is a rent check from a tenant. This rent is DOC’s main source of revenue.

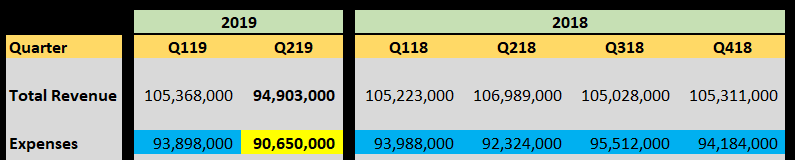

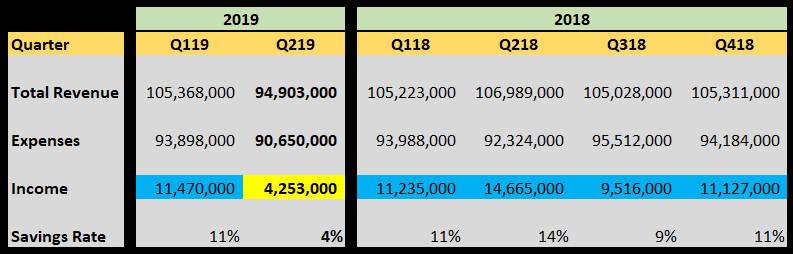

So let’s take a look at DOC’s revenue from the last six quarters. The average is $103.8 million and the most recent quarter came in at about $95 million (yellow).

As you can see, due to some tenant issues, Physicians Realty Trust only grossed about $95 million in revenue during the quarter ending 6/30/2019 as compared to the $105 million in revenue they usually gross. We normally see some consistency here, but this quarter took a hit on revenue. We should see this bounce back next quarter and we might even have the opportunity to re-capture come of the lost revenue in the future that resulted from our tenant issues.

Unfortunately, Physicians Realty Trust and I, as a shareholder, do not get to keep all of that rent and revenue. That’s because there are expenses that come along with owning medical office buildings that we need to back out first.

REIT Expenses

Just like owning a traditional house, when we own medical office buildings, we are going to have expenses. Expenses resulting from things like building maintenance, interest, taxes, insurance, and administrative costs for things like paying the bills. Yes, there is a cost (time) when someone is managing a household and paying bills. I generally account for my time at about $30/hour so the more I automate in my own household the better. DOC probably has a whole department dedicated to managing the administrative tasks tied to owning 250 buildings. Think about how all the rules and regulations might vary from one state to another; someone has to figure all that stuff out.

DOC breaks their expenses into four very specific categories on their income statement, but we won’t dive too deep into those categories here.

- Interest Expense

- General and Administrative

- Operating Expenses

- Depreciation and Amortization

Healthcare REITs take a depreciation expense to represent a decrease in the value of the buildings as required by GAAP. This is an expense someone like Max OOP probably doesn’t account for in our own household because real estate generally goes up at the rate of inflation or more. I mentioned this briefly when I got ahead of myself and discussed DOC’s Funds from Operations (FFO) earlier this year.

Physicians Realty Trust’s total expenses over the last six quarters have been hovering at about $93.4 million per quarter but dropped this last quarter to $90.6 million.

Healthcare REIT Income

Income is nice for math teachers like Mrs. Max OOP because we get to use an equation. In this particular equation, we take revenue minus expenses to get our income.

Revenue – Expenses = Income

We can actually plug in our variables from above to come up with DOC’s income for the second quarter of 2019 ending 6/30/2019.

$94.9 million revenue – $90.6 million expenses = $4.3 million income

So DOC’s quarterly income for the quarter ending 6/30/2019 was about $4.3 million dollars. This comes out to a “savings rate” of about 4.48%. They usually run about 11% so this wasn’t a great quarter mostly due to our tenant issues. There is a pretty cool footnote in their financial statements that I won’t review here, but I am expecting some of that revenue to come back in a future quarter. Here is the income from the last six quarters.

Here is a nice look at the same information directly from their 2019 Q2 supplemental.

Final Thoughts

If you are going to run an experiment, it is good to understand the fundamentals. Healthcare REITs can get complex, but in the end, they run just like any other business or household. When you look at a granular business like this, it is almost easier to understand than the total stock market index. I know all the companies in the stock market are trying to make money and do a great job at it. But seeing revenue, expenses, and income in action at a company level like this is nice. Getting to touch the dividends that result is even better.

Now there are certainly more variables to consider. For example, one thing that can often impact income is the sale of a medical office building where DOC makes money on the sale. Those transactions are not included in the numbers above. But just looking at these operating numbers can give us a pretty good idea where things stand.

I have always wanted to completely dissect a company that I don’t work for, and I am doing that now. I am exposing myself to risk in doing so, but it is also just a small sliver of my portfolio. Expensive hobby? Maybe. I am staying with DOC at this point because I think management has handled the tenant issues and may even be positioned to recapture some of that revenue.

REIT Experiment Update

This is my first post on the experiment since August 6th when I discussed where I am keeping all of these medical office buildings. Since then I have invested another $2,900 into healthcare REITs through DOC. These happened through two separate transactions on 8/16/2019 and 8/30/2019. This medical office building investment is projected to net about $1,700 in dividends over the next 12 months, and in total is worth just north of $31,000. The last few transactions have been through my brokerage account since we want to see how the taxes on about $100 in dividends will hit my 2019 tax return.

I forgot to buy DOC yesterday! It was really busy at work yesterday and I was emersed in several different projects and all of a sudden it was after 4 pm and the market was closed. I usually try to squeeze this type of business in on my lunch break, but I just forgot. So I will either make an off-cycle purchase on Monday or pool the money for two weeks and roll it into my next purchase. Here is where we stand:

Healthcare REITs: Where Do We Go From Here?

I mentioned during my August update that I was likely going to slow down my coverage of the healthcare REIT experiment but continue to dollar-cost average into it every payday throughout the rest of the year. My post frequency will likely drop to about monthly. I am considering building this portfolio up to the point to where I can cover my max out-of-pocket costs in any given year with the dividends it generates. It would technically be a partial form of ‘healthcare financial independence’ and completely separate from my overall retirement portfolio. I am starting to think there might be some advantages to carving out our healthcare costs and developing a unique portfolio to deal with them. I expect we will continue to see out-of-pocket healthcare costs in the United States, even in a Medicare For All scenario.

As of today, my ‘one stock’ healthcare REIT portfolio and its $1,700 in dividends will cover about 25% of my 2019 max out-of-pocket. My 2019 max out-of-pocket comes in at $6,600 and will likely increase again in 2020 so I will need to adjust the goal at that point. As of today, our 2019 out-of-pocket costs for healthcare are holding at $0.00, not including premiums. We are lucky to be healthy.

Usual disclaimer: This is not a recommendation to buy this or any other stock/healthcare REIT. You are responsible for your own investment decision and buying a single undiversified stock like this is almost never a good idea.

The post Healthcare REITs: Back To The Basics appeared first on Max Out of Pocket.

]]>The post Where Do I Keep All Of These Medical Office Buildings? appeared first on Max Out of Pocket.

]]>Deprecated: ltrim(): Passing null to parameter #1 ($string) of type string is deprecated in /home/wilbul4/maxoutofpocket.com/wp-includes/wp-db.php on line 3030

If you need to catch up, Max OOP has slowly built up a healthcare REIT investment called Physicians Realty Trust (DOC) to just over $28,000. DOC primarily makes me money by owning and renting out medical office buildings to organizations that provide direct medical care. As of the beginning of August, this investment is projected to earn me about $1,500 in passive income over the next 12 months. This happens even while I am doing fun things like checking out the highest tides in the world or taking photos of lupines in northern New Hampshire.

We have not pulled the trigger on early retirement yet, so we spent some time a few weeks back busting tax brackets to make sure we understand how our income gets taxed. We found Mrs. Max OOP and I are still getting taxed about 22 cents on the dollar in federal income taxes for each additional taxable dollar we add to our income bucket. So we need to be really careful when we build a healthcare REIT money machine that spits out quarterly dividends on a conveyor belt right back into my pocket four times per year. We don’t have to worry about Medicare FICA or Social Security FICA at our income level since those taxes don’t apply to unearned income. But we do have to worry about regular federal income taxes. We don’t want the federal government reaching into my pocket and taking 22% of those ‘rental dividends’ since that can really hurt my ability to grow the portfolio and retire early. We would rather take that 22% and invest it for additional gains.

Ordinary Dividends

For the sake of simplicity, I was hoping we could just assume all of DOC’s dividends are what we like to call, ordinary dividends. But in reality, in 2018 only about 30% of the dividends Physicians Realty Trust released were considered ordinary dividends and the rest is what they call “non-dividend distributions”. We are going to dig into the difference between these in a later post, but for now, I am going to zero in on the fact that DOC’s dividends are both ordinary and a bit complex. As a general rule, usually Max OOP doesn’t like ordinary or complex, and that rule of thumb applies to these dividends.

The bad thing about ordinary dividends is they are taxed like ordinary income and land in the ordinary earned income federal tax buckets. I like to compare these ordinary dividends with earned income someone might earn from their regular day job. If the REIT dividend was a qualified dividend, it would be taxed at a much lower rate (0%, 15%, or 20%).

We won’t get too deep into the definition of a qualified dividend here, but generally, REIT dividends just don’t meet the IRS requirements to be considered a qualified dividend. That makes them non-qualified, or just ordinary dividends.

These ordinary dividends can become unfavorable if someone like Max OOP is still working and sitting in a higher tax bucket. In my case, the ordinary dividends put back into my pocket by DOC would be taxed at 22%. This is not ideal and can quickly turn my $1,500 in annual income into only $1,170 once I settle up with my Uncle Sam. That would be a sad story, so I am not going to let that happen.

$1,500 ‘REIT rental dividends’ X 22% = $330 Tax

$1,500 – $330 = $1,170 left in my pocket

Simplify Life

Max OOP doesn’t want to have to worry about a 22% tax on the ordinary dividends issued by DOC, or the tax treatment of these confusing “non-dividend distributions”. So I do what I always do; take a simple way out. I hold all of my medical office buildings in either a Roth IRA account or a Traditional IRA Account.

Roth IRA Bucket

My Roth IRA offers tax-free growth for all my investments in that account. This includes medical office buildings held in the form of REITs. In other words, there will be no taxes applied to assets in these accounts when they are withdrawn in retirement or dividends that are issued over the years. In even more words, assets in this account are sheltered from federal taxes kind of like our healthcare premiums are when we buy them from our cafeteria plan. This is because those dollars were taxed at the time I earned them from my day job. I put those dollars into this Roth IRA account with special abilities to shelter us from taxes. Then I took those dollars and invested them into medical office buildings. There are a lot of other superpowers that come along with an account like this, but the main takeaway here is I will never need to worry about how the dividends in this account are taxed. Ordinary shmordinary, the federal income tax just doesn’t apply to assets in this account. My Roth IRA account currently holds about $7,400 of the Max Out of Pocket REIT portfolio. So about $400 of my annual dividend income (as of August 2019) will land in this Roth IRA bucket and thus never land in the 22% tax bucket. Thus they will never be taxed.

Here is that position as of August 2nd:

I suppose I technically can’t predict the future and the government could change the tax rules someday, but I will go out on a limb and say that is extremely unlikely. That said, I am sure the last Czars of Russia thought it was extremely unlikely the entire family would be massacred, but it happened.

Traditional IRA Bucket

My traditional IRA account holds assets where the taxes are deferred until the assets are withdrawn. I still earned these dollars from my day job, they just weren’t taxed at the time I earned them. I diverted them to this special traditional IRA account. They were essentially deducted (subtracted) from my gross income the year they were earned. When they are withdrawn, they will be taxed as ordinary income. This will hopefully occur at a time when I am in a much lower tax bracket and not getting taxed 22 cents on the dollar. The key takeaway here is I don’t need to worry about getting taxed on these dividends until way in the future, so no tax will be applied to this dividend income in the year I receive the dividend. My IRA bucket holds about $14,000 of the Max Out of Pocket Healthcare REIT portfolio and will generate about $1,000 in passive income over the next year.

Here is that position:

Brokerage Bucket

My position of DOC (Physicians Realty Trust) held in my brokerage account at the end of the month was $0.00. Ordinary dividends that land in this bucket are considered part of ordinary income and would be subject to regular federal income tax rates as determined by our tax bracket. About 30% of DOC’s dividends are considered ordinary. Since that would mean a 22% tax for Max OOP, so far I have just opted out of using this bucket for holding any of the Max Out of Pocket Healthcare REIT portfolio.

I do have some homework to do here, though. Since only about 30% of Physicians Realty Trust’s dividends are considered ordinary, we do need to get a better understanding of how the other 70% “non-dividend distributions” are handled. So since Friday was payday, I went ahead and made my usual purchase of Physicians Realty Trust. But this purchase was a little different; I squeezed these medical office buildings into my brokerage account. That way we can follow these through to our 2019 tax return. Look at that, I am willing to complicate my life a little bit in the name of Max Out of Pocket.

We will probably need to slow this experiment down soon since the initial plan was to consider holding the portfolio at $25,000. Max OOP has always struggled to stay on track with things.

Final Thoughts